Ship Mortgages: How Lenders Secure Financing and What Covenants Protect Them

- Dushyant Bisht

- Mar 30

- 10 min read

Key Takeaways

Ship mortgage registration process requires filing with flag state registries to establish the ship mortgage as public notice of the lender's security interest, with first-registered mortgages receiving priority over subsequent mortgages on the same vessel under maritime collateral rules

Preferred mortgage versus statutory mortgage priority determines whether ship mortgages rank ahead of maritime liens, with U.S. preferred ship mortgages receiving priority over most liens except crew wages while ordinary mortgages typically rank subordinate to all maritime liens

Ship mortgage covenants and defaults include financial covenants requiring minimum loan-to-value ratios and debt service coverage, operational covenants mandating insurance and classification maintenance, negative covenants prohibiting additional liens, and cross-default provisions making defaults on other obligations trigger mortgage defaults

Enforcement of a ship mortgage occurs when lenders seek vessel arrest for mortgage enforcement through admiralty courts following payment defaults or covenant breaches, leading to foreclosure and judicial sale with proceeds distributed according to the priority of ship mortgages and competing maritime claims

Discharge of ship mortgage requires full debt repayment followed by filing mortgage discharge documentation with the flag state registry to release the lender's security interest and clear the vessel's title for sale, refinancing, or other ownership transactions

What You'll Learn in This Article

Most ship acquisitions require debt financing since vessels cost tens of millions to hundreds of millions of dollars. Ship mortgages provide lenders with security interests in vessels, enabling ship finance markets to function. These mortgages operate differently from real estate mortgages due to ships' mobile nature and exposure to maritime liens. This article explains what ship mortgages are, how registration works, what covenants protect lenders, how enforcement occurs when borrowers default, and what mortgage structures mean for ship investors.

Understanding ship mortgages clarifies how debt financing affects vessel ownership and the balance between owner flexibility and lender security.

What Is a Ship Mortgage?

A ship mortgage is a consensual security interest granted by a shipowner to a lender as collateral for a loan. The mortgage creates a lien on the ship, giving the lender rights to enforce against the vessel if the borrower fails to repay the debt according to agreed terms (1).

Ship mortgages function similarly to real estate mortgages in providing secured financing. The borrower receives loan proceeds and pledges the asset as security. If repayment occurs on schedule, the lender eventually releases the mortgage. If the borrower defaults, the lender can seize and sell the asset to recover the debt.

However, ships differ fundamentally from real estate in ways affecting mortgage mechanics. Ships move between jurisdictions, operate in international waters, and can be hidden or sold quickly. These characteristics require ship mortgages to include specific provisions addressing mobility, international enforcement, and rapid asset disposition risks.

Ship mortgages also face competition from maritime liens that can have priority over the mortgage despite being created afterward. As explained in our maritime liens article, crew wages, salvage claims, and other maritime liens often rank ahead of mortgages. This subordination risk distinguishes ship mortgages from real estate mortgages where properly recorded first mortgages typically have uncontested priority (2).

The legal framework for ship mortgages varies by flag state. Each country's maritime laws govern mortgage creation, registration, priority, and enforcement for ships flying its flag. International conventions provide some harmonization, but significant variation remains across jurisdictions.

How Does Ship Mortgage Registration Work?

Ship mortgage registration occurs with the flag state registry where the vessel is documented. Flag states maintain ship registries recording vessel ownership, tonnage certificates, and encumbrances including mortgages. Registration provides public notice that the mortgage exists, establishing the lender's security interest and priority position.

The registration process requires submitting the mortgage deed, identifying the vessel by official number and name, specifying the debt amount secured, and paying registry fees. The registry records the mortgage chronologically, with first-registered mortgages receiving first priority among competing mortgages on the same vessel.

First mortgage priority matters significantly. If multiple lenders have mortgages on one ship, the first-registered mortgage gets paid first from enforcement proceeds. Second and subsequent mortgages receive payment only if proceeds exceed the first mortgage amount. This priority system incentivizes lenders to search registries before lending and to record mortgages immediately upon closing (3).

International recognition of ship mortgages facilitates enforcement across jurisdictions. Most maritime nations recognize properly registered foreign ship mortgages, allowing lenders to enforce in courts beyond the flag state. This recognition enables global ship finance where Greek banks finance Panama-flagged ships trading worldwide with enforcement available wherever the ship calls.

Some registries offer online access to mortgage records, improving transparency. Major open registries including Panama, Liberia, and Marshall Islands maintain searchable databases showing recorded mortgages. However, registry practices vary, with some countries providing limited public access to mortgage information.

De-registration protections prevent borrowers from evading mortgages by changing flag states. Legitimate registries refuse to register ships with outstanding recorded mortgages from the previous registry unless mortgagees provide written consent. This protection prevents borrowers from "flag hopping" to escape lender security.

What Is a Preferred Ship Mortgage?

Preferred ship mortgages exist under United States maritime law, providing mortgagees with priority over most maritime liens except crew wages. This preferred status gives U.S. maritime lenders stronger security than mortgages in jurisdictions where all maritime liens have priority over mortgages (4).

To qualify as a preferred mortgage, specific requirements must be met. The vessel must be documented under U.S. flag with the Coast Guard. The mortgage must be recorded with the National Vessel Documentation Center. The mortgage instrument must be executed and acknowledged according to statutory requirements. Only mortgages meeting these conditions receive preferred status.

Preferred mortgage priority ranks behind crew wage liens but ahead of salvage liens, necessaries liens, and other maritime claims. This middle position balances seafarer protection policy with lender security needs. A preferred mortgage on a U.S.-flagged ship provides substantially better security than an ordinary mortgage on a foreign-flagged ship where the mortgage ranks behind all maritime liens.

The preferred mortgage concept reflects U.S. policy encouraging domestic ship finance. By providing lenders with better security, preferred mortgage status reduces lending risk and potentially lowers financing costs for U.S.-flagged ships. However, the requirement to flag vessels in the U.S. limits preferred mortgage benefits to domestic registry ships.

Outside the United States, preferred mortgage equivalents are rare. Most jurisdictions maintain traditional maritime law where maritime liens have blanket priority over mortgages. This international variation means mortgage priority depends heavily on flag state selection, influencing both registry choice and financing terms.

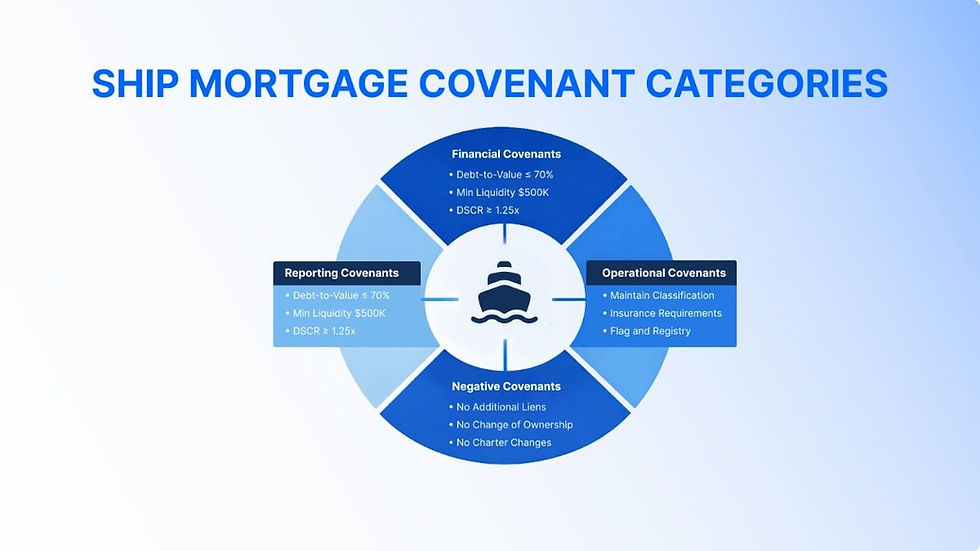

What Covenants Do Ship Mortgages Contain?

Ship mortgage covenants are contractual provisions requiring borrowers to maintain specific conditions and prohibiting certain actions without lender consent. These covenants protect lender security by ensuring the mortgaged ship maintains value and remains available for enforcement if default occurs.

Financial Covenants

Loan-to-value ratio covenants require maintaining minimum vessel value relative to outstanding debt. A typical covenant might require the ship's market value to remain at least 125% of the loan balance. If the ship depreciates or debt repays slowly, the borrower must make additional principal payments to restore required loan-to-value ratios (5).

Debt service coverage requirements ensure operating cash flows exceed debt payments with adequate cushion. Lenders commonly require charter revenues to cover debt service by at least 1.25 to 1.5 times. This protects against revenue volatility causing payment defaults.

Minimum liquidity covenants require borrowers to maintain cash reserves covering several months of debt service. This provides a buffer against temporary revenue interruptions from technical problems, market downturns, or operational disruptions.

Operational Covenants

Insurance covenants require maintaining hull and machinery insurance covering the ship's mortgaged value, naming the lender as loss payee or additional insured. This ensures insurance proceeds from total loss flow to the lender rather than the borrower. Protection and indemnity insurance covering third-party liabilities is also typically required.

Classification society covenants mandate keeping the ship in class with an approved classification society. Loss of class indicates serious technical problems or deferred maintenance, threatening ship value and operation. Lenders require immediate notification of class suspensions or withdrawals.

Trading area restrictions limit where the ship can operate. Mortgages typically prohibit trading in war zones, high-risk piracy areas, or regions where insurance coverage is unavailable or expensive. Geographic restrictions protect ship value by avoiding high-risk operations (6).

Maintenance covenants require maintaining the ship in good condition according to manufacturer recommendations and classification society requirements. Deferred maintenance reduces ship value and creates operational risks. Some mortgages require minimum annual maintenance spending.

Negative Covenants

No additional liens covenants prohibit creating new security interests without lender consent. This prevents borrowers from subordinating the mortgage or depleting equity through additional borrowing. However, these covenants typically permit maritime liens arising from normal operations since such liens are unavoidable.

Charter restrictions require lender approval for time charters exceeding certain durations. Long-term charters at below-market rates can impair ship value. Lenders want to review charter terms ensuring they don't harm collateral value or provide opportunities for borrower misconduct.

Sale and disposal restrictions prohibit selling the ship or major equipment without lender consent and full debt repayment. This prevents borrowers from disposing of collateral without satisfying the mortgage.

Flag and registry covenants prohibit changing the ship's flag state without lender approval. Flag changes can affect mortgage enforceability, priority, and lender remedies. Lenders typically restrict flags to approved maritime jurisdictions with established legal systems.

Reporting Requirements

Financial reporting covenants require regular submission of financial statements, charter contracts, insurance certificates, and operational reports. Quarterly or monthly reporting is common, enabling lenders to monitor covenant compliance and identify problems early.

Immediate notification requirements obligate borrowers to report major casualties, arrests, regulatory violations, classification issues, or other events materially affecting the ship. Timely notification allows lenders to protect their security before situations deteriorate.

What Constitutes Default and How Do Lenders Enforce?

Payment default occurs when borrowers fail to make principal, interest, or fee payments when due. Most mortgages allow brief cure periods (typically 3-10 days) before payment defaults trigger acceleration rights. After cure periods expire without payment, lenders can declare entire loans immediately due and payable.

Covenant breaches constitute defaults even without missed payments. Violating loan-to-value ratios, losing insurance coverage, allowing classification to lapse, or trading in prohibited areas can trigger defaults. Most mortgages distinguish between payment defaults and covenant defaults, allowing longer cure periods for covenant breaches.

Cross-default provisions make defaults under other debt agreements also defaults under the mortgage. If a borrower defaults on obligations to other lenders, mortgage lenders can declare their loans in default even if all mortgage payments are current. Cross-defaults protect lenders from subordination to other creditors during financial distress (7).

Enforcement mechanisms vary by jurisdiction but typically include ship arrest and judicial sale. The lender applies to admiralty courts for arrest warrants based on mortgage default. Once arrested, the ship cannot operate until the default cures or security posts. If default continues, courts order judicial sale with proceeds distributed according to priority.

Foreclosure procedures resemble real estate foreclosure but occur in admiralty courts under maritime law. The ship sells at public auction with the lender entitled to bid. Judicial sales often realize below-market prices since buyers acquire ships under legal cloud with limited inspection periods and uncertain condition.

Out-of-court resolutions sometimes occur through negotiated sales where borrowers voluntarily sell ships with lender cooperation. This can produce better prices than forced judicial sales while avoiding litigation costs. However, lenders retain judicial enforcement as ultimate remedy when cooperation fails.

How Are Ship Mortgages Discharged?

Mortgage discharge occurs when the secured debt is fully repaid and the lender releases its security interest. The borrower makes final payment, and the lender executes a satisfaction of mortgage document acknowledging full repayment and releasing all claims against the ship.

Registry discharge requires filing the satisfaction document with the flag state registry where the mortgage was recorded. The registry updates records showing the mortgage is discharged, clearing the ship's title of the lien. This public recordation enables the owner to sell, refinance, or otherwise deal with the ship free of the discharged mortgage.

Timing matters when coordinating debt repayment with ship sales or refinancing. Buyers or new lenders require evidence that existing mortgages will discharge at closing. Closing procedures typically use escrow arrangements where sale or refinancing proceeds pay off existing mortgages simultaneously with title transfer or new mortgage recording.

Partial discharge can occur when multiple ships secure one loan and the borrower repays sufficient principal to justify releasing individual ships from the collateral pool. Lenders evaluate whether remaining collateral adequately secures the reduced debt balance before agreeing to partial releases (8).

Documentation is critical for mortgage discharge. Lost or destroyed original mortgages require legal proceedings to establish satisfaction. Lenders should maintain careful records of mortgage documents and borrower payment history to facilitate smooth discharge when loans are repaid.

Conclusion

Ship mortgages represent the primary vessel mortgage financing mechanism enabling shipowners to acquire and operate maritime assets while providing lenders with ship financing security through maritime collateral. Understanding the ship mortgage registration process, including flag state registration requirements and first mortgage priority principles, is essential for both borrowers and lenders navigating international ship finance. Ship mortgage covenants and defaults create the contractual framework protecting lender interests through financial covenants like loan-to-value ratios, operational requirements, and negative covenants restricting additional liens or flag changes.

The priority of ship mortgages relative to maritime liens varies significantly by jurisdiction, with preferred mortgage status under U.S. law providing better security than statutory mortgages subordinate to all maritime liens. Whether through enforcement of a ship mortgage via vessel arrest and judicial sale, or through discharge of ship mortgage upon debt satisfaction, the mechanics of maritime secured lending require specialized knowledge of admiralty law, cross-default provisions, and international registry practices to effectively balance shipowner flexibility with lender protection.

COMPLIANCE DISCLAIMER:

This content is for informational and educational purposes only. It does not constitute legal advice, financing guidance, or lending recommendations. Ship mortgage law, registration requirements, covenant terms, enforcement procedures, and lender rights vary significantly by flag state, jurisdiction, and specific loan agreements. Mortgage terms, conditions, and enforceability differ substantially between transactions, lenders, and legal systems. This article provides general information only and should not be relied upon for specific financing or legal decisions. Readers should consult qualified maritime lawyers, ship finance advisors, and legal counsel in relevant jurisdictions for advice on ship mortgages, maritime security interests, and related matters.

FAQs on Ship Mortgage

What is a ship mortgage?

A ship mortgage is a consensual security interest granted by a shipowner to a lender as collateral for a loan. The mortgage gives the lender rights to enforce against the ship if the borrower defaults, including the right to arrest the vessel and force judicial sale to recover the debt.

How is a ship mortgage registered?

Ship mortgages are registered with the ship's flag state registry where the vessel is documented. Registration provides public notice of the mortgage and establishes priority among competing claims. First-registered mortgages typically have priority over later mortgages on the same ship.

What is a preferred ship mortgage?

A preferred ship mortgage under U.S. law is a mortgage on a U.S.-flagged ship that meets specific statutory requirements and receives priority over most maritime liens except crew wages. This gives lenders better security than ordinary mortgages subordinate to all maritime liens.

What covenants are typical in ship mortgage agreements?

Typical covenants include maintaining insurance, keeping the ship in class, trading in approved areas, maintaining minimum loan-to-value ratios, providing financial reports, obtaining lender consent for charters, and prohibiting additional liens. Covenants protect lender security by ensuring the ship maintains value.

How do lenders enforce ship mortgages when borrowers default?

Lenders can arrest the mortgaged ship through admiralty courts, preventing it from trading. The court can order judicial sale with proceeds distributed to creditors according to priority. Foreclosure proceedings vary by jurisdiction but generally result in forced asset sale to satisfy the debt.

Dushyant Bisht

Expert in Maritime Industry

Dushyant Bisht is a seasoned expert in the maritime industry, marketing and business with over a decade of hands-on experience. With a deep understanding of maritime operations and marketing strategies, Dushyant has a proven track record of navigating complex business landscapes and driving growth in the maritime sector.

Email: [email protected]