Alternative Investments: Definition, Types, Advantages, and Disadvantages (2026 Guide)

- Ravi Shankar FICS

- Apr 12, 2023

- 14 min read

Updated: Jun 23

The first time I encountered the term "alternative investments" in a professional context was at a conference on maritime asset financing in Singapore. The room was full of fund managers discussing infrastructure assets, private credit, and real assets, all of them using "alternatives" as shorthand for everything that was not a publicly listed stock or a government bond. That shorthand is useful, but it conceals enormous variety.

A hedge fund and a ship are both "alternative investments." Understanding what they have in common, and how they differ, is the starting point for any serious evaluation.

Quick Answer: What Are Alternative Investments? Alternative investments are asset classes that fall outside the traditional categories of publicly traded stocks, bonds, and cash. The category includes private equity, hedge funds, real estate, commodities, infrastructure, private credit, and real assets such as art, timber, and commercial vessels. They share several characteristics: lower liquidity than public market assets, limited correlation with equity markets, and typically higher minimum investment requirements. Alternatives are used by institutional investors and high-net-worth individuals primarily for portfolio diversification and return enhancement.

What Are Alternative Investments?

Traditional investments are publicly traded: stocks listed on exchanges, government and corporate bonds traded in liquid markets, and cash or money market instruments. They are accessible to retail investors, priced daily, and regulated by securities authorities that mandate disclosure.

Alternative investments are everything else. The category is defined negatively: not publicly traded in the conventional sense, not directly correlated with the stock or bond market, and not governed by the same regulatory framework as public securities.

This definition encompasses an enormous range of assets: from a buyout fund acquiring a manufacturing company, to a hedge fund running quantitative trading strategies, to a direct investment in agricultural land, to an economic interest in a commercial vessel. What unites them is structural rather than sectoral: they are accessed through private arrangements rather than public exchanges.

The alternative investment market has grown substantially over the past two decades. The global alternatives market was estimated at approximately $16 trillion in assets under management in 2024, with private equity and real assets accounting for the largest shares. Institutions including pension funds, sovereign wealth funds, insurance companies, university endowments, and family offices are the primary allocators to alternatives. The Yale University endowment, which pioneered large-scale institutional allocation to alternatives in the 1990s under David Swensen, achieved annualised returns significantly above the traditional 60/40 equity-bond portfolio over multiple decades.

Retail access to alternatives has expanded but remains constrained by regulation. In the US, the accredited investor standard (individual net worth above $1 million excluding primary residence, or annual income above $200,000) governs who may invest in unregistered private offerings. VARA regulation in the UAE and MAS regulation in Singapore apply analogous frameworks to digital asset investment products.

The Main Types of Alternative Investments

Private Equity

Private equity (PE) involves taking ownership stakes in companies that are not publicly listed. The main PE strategies are:

Buyout: Acquiring a controlling stake in an established company, typically using significant debt (leveraged buyout or LBO). The PE firm works with management to improve the business over 3 to 7 years, then exits through a sale or initial public offering (IPO).

Growth equity: Taking a minority stake in a growing company that does not yet require the full operational transformation a buyout involves. Less control, less debt, focus on organic growth support.

Venture capital: Early-stage investment in startups. High risk (most portfolio companies fail) offset by the potential for exceptional returns from the few that succeed at scale.

Private equity is characterised by: illiquidity (capital is locked up for the fund's life, typically 7 to 10 years), high minimum commitments (typically $1 million to $10 million for institutional fund entry), and fee structures (the standard "2 and 20" model charges a 2% management fee and 20% carried interest on profits above the hurdle rate).

Hedge Funds

Hedge funds are pooled investment vehicles that use a wide range of strategies to generate returns, including short selling, leverage, derivatives, and arbitrage, which are not available to conventional mutual funds. Major strategy categories include:

Long/short equity: Taking long positions in stocks expected to rise and short positions in stocks expected to fall.

Global macro: Making directional bets on currencies, interest rates, commodities, and equity indices based on macroeconomic analysis.

Quantitative/systematic: Using algorithms and statistical models to identify and exploit market inefficiencies at high frequency.

Event-driven: Trading around corporate events: mergers, bankruptcies, spin-offs, restructurings.

Hedge funds charge similar fees to PE (historically 2 and 20, though competitive pressure has reduced this), typically require significant minimum investments, and offer quarterly or annual liquidity rather than daily redemption.

Real Estate

Real estate alternatives span a wide range from direct property ownership to pooled vehicles:

Direct real estate: Purchasing commercial or residential property directly. The largest alternative asset by total value globally.

Real estate investment trusts (REITs): Pooled vehicles holding real estate assets. Listed REITs trade on stock exchanges; non-listed REITs are private. Listed REITs are sometimes considered hybrid assets rather than pure alternatives because of their stock exchange liquidity.

Private real estate funds: Closed-end funds acquiring commercial property (offices, logistics facilities, retail, residential) on behalf of investors. Structure similar to PE: drawdown capital, 5 to 10-year life, carried interest.

Real estate debt: Providing loans secured against real estate. Mezzanine debt (subordinated) commands higher rates than senior debt.

Infrastructure

Infrastructure investments cover physical assets that provide essential services: transport (ports, airports, toll roads, railways), utilities (water, power transmission, pipelines), energy (renewable power generation, LNG terminals), and digital infrastructure (data centres, fibre networks).

Infrastructure assets typically have long operational lives (30 to 100 years), regulated or contracted revenue streams, high barriers to entry, and low correlation with equity markets. They are favoured by pension funds and insurance companies that need to match long-duration liabilities with long-duration assets.

Maritime infrastructure (ports, terminals, shipyards) falls within this category and represents a segment of the alternatives market with direct relevance to the Shipfinex platform's focus on maritime assets.

Private Credit / Private Debt

Private credit is lending to companies or projects outside the public bond market. It emerged significantly after the 2008 global financial crisis reduced banks' appetite for certain types of corporate lending.

Major subcategories include direct lending (senior secured loans to mid-market companies), mezzanine debt (subordinated, higher-yielding), distressed debt (loans to financially stressed or defaulted borrowers), and trade finance.

Private credit offers investors floating-rate returns (as most loans are variable rate), security over assets, and yields that typically exceed equivalent public market fixed income. Illiquidity is the key trade-off.

Commodities

Commodity investments provide exposure to physical raw materials: agricultural products, energy resources, precious and industrial metals, and timber. Commodities can be accessed directly, through futures contracts, through commodity-focused funds, or through commodity producer equities.

The primary value of commodity exposure in a portfolio context is its historically low or negative correlation with equity and bond markets, making it a potential hedge against inflation and equity downturns.

Real Assets (Hard Assets)

Beyond real estate and infrastructure, real assets include:

Timber and farmland: Long-duration, inflation-linked returns; illiquid; requires specialist management.

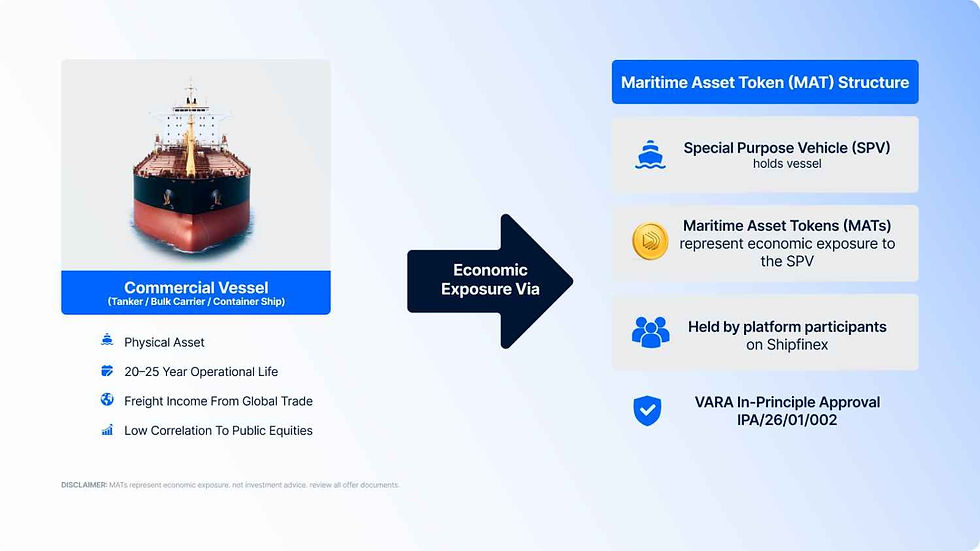

Maritime assets: Commercial vessels (tankers, bulk carriers, container ships) generate freight income correlated with global trade volumes rather than equity markets. Investment can be accessed through direct vessel ownership, shipping company equity, shipping debt, or increasingly through tokenised maritime asset structures.

Art and collectibles: Wine, art, classic cars, watches. Illiquid; no yield; return depends entirely on value appreciation; expert knowledge required.

Precious metals (direct): Physical gold and silver held as a store of value; no yield; low correlation with equities in stress periods.

Asset Class | Liquidity | Typical Hold | Min. Entry | Key Driver | Correlation to Equities |

Private equity | Very low | 5-10 years | High | Business performance | Low |

Hedge funds | Low-medium | Quarterly/annual | High | Strategy execution | Varies |

Real estate | Low | 3-10 years | Medium-high | Property values, rents | Low-medium |

Infrastructure | Very low | 10-30 years | Very high | Contracted revenues | Very low |

Private credit | Low | 2-7 years | High | Interest rates, credit quality | Low |

Commodities | Medium | Flexible | Low-medium | Supply/demand cycles | Low |

Maritime assets | Low-medium | 5-15 years | Medium | Freight markets, trade volumes | Very low |

Art/collectibles | Very low | Long-term | Varies | Demand, provenance | Near zero |

Advantages of Alternative Investments

Portfolio Diversification

The primary argument for alternatives is that they have historically shown low correlation with public equity and bond markets. When equity markets sell off sharply (as in 2008, 2020, and 2022), assets with different economic drivers do not necessarily follow the same trajectory.

Infrastructure assets with contracted revenues continue earning their returns regardless of equity market sentiment. Commodities may rise during inflationary periods that push bond prices down. Maritime assets respond to freight market supply and demand, which is driven by global trade volumes and fleet capacity, not by listed company earnings.

True diversification: assets that perform differently during periods of equity market stress, not assets that simply have lower volatility than equities.

Return Enhancement

Alternatives offer a structural return premium in exchange for illiquidity. This "illiquidity premium" compensates investors for the fact that they cannot sell their position at will. Private equity returns have, over long periods and across multiple market cycles, exceeded public equity returns for top-quartile managers.

Private credit yields typically exceed equivalent public market fixed income. Infrastructure assets in regulated sectors offer stable, predictable returns that outperform cash over long periods.

Inflation Hedging

Real assets (real estate, infrastructure, commodities, agricultural land) tend to maintain or grow their value in inflationary environments. Infrastructure assets with revenue indexed to inflation (common in regulated utility and toll road structures) pass inflation directly to investors through higher revenues. Commodities rise in price during supply-driven inflation.

Access to Private Market Returns

A large proportion of global economic activity occurs in private companies that never list on public markets. Private equity and venture capital provide access to this universe of companies, which is increasingly where high-growth businesses choose to remain.

Lower Volatility (Structural, Not Market)

Private asset valuations are not marked to market daily. A private equity fund's quarterly valuation is an assessed fair value, not a continuous market price. This means reported volatility is lower than for publicly traded equivalents, though the underlying economic risk is not necessarily lower. Investors must understand this distinction.

Disadvantages of Alternative Investments

Illiquidity

Most alternative investments cannot be sold quickly. A PE fund commitment is locked for the fund's life. Infrastructure assets require years to exit. Even hedge funds with quarterly redemption windows impose notice periods and sometimes suspension of redemptions in stressed market conditions.

For investors who may need access to capital unexpectedly, illiquidity is a genuine constraint. Portfolio construction for alternatives investors must account for liquidity needs over the investment horizon.

High Minimum Investment Requirements

Most institutional alternative investment vehicles require minimum commitments of $1 million to $10 million or more. This restricts access to institutions and high-net-worth individuals. Platforms that tokenise alternative assets or aggregate them into accessible structures (REITs, listed infrastructure funds) can lower this threshold, but introduce their own structural considerations.

Complexity and Due Diligence Burden

Evaluating a private equity fund requires understanding its investment strategy, the track record of its specific team, its fee structure, the quality of its portfolio company pipeline, and its exit history. Evaluating a maritime asset investment requires understanding the freight market dynamics, the vessel's age and condition, the charter party terms, and the operator's management quality. These assessments require specialist knowledge.

Fee Structures

The "2 and 20" model (or variations thereof) means that a significant portion of gross returns is captured by the manager rather than the investor. At a 2% annual management fee and 20% carried interest, a fund generating 15% gross returns delivers approximately 11% to investors (before considering the hurdle rate and specific fee arrangements). High fees require high gross performance to justify.

Lack of Transparency

Private fund investments provide quarterly reports rather than daily pricing. Information disclosed may be limited compared to public company regulatory disclosures. Due diligence on private assets requires accessing information that is not publicly available.

Regulatory and Legal Complexity

Alternative investments are typically structured as limited partnerships, closed-end funds, or special purpose vehicles in jurisdictions including the Cayman Islands, Luxembourg, or Delaware. Understanding the legal structure, the tax treatment, the governance rights of limited partners, and the circumstances under which the manager's decisions can be challenged requires specialist legal and tax advice.

Valuation Uncertainty

Private assets do not have continuous market prices. Valuation is an assessment, conducted quarterly or less frequently, using methods including comparable company analysis, discounted cash flow, and recent transaction multiples. Different assumptions produce different valuations. During periods of market stress, the reliability of private asset valuations is a legitimate concern.

Alternative Investments and Maritime Assets

The maritime sector offers an alternative investment category that combines characteristics of infrastructure, real assets, and commodities. Commercial vessels are capital-intensive physical assets with long operational lives (20 to 25 years for a modern bulk carrier or tanker) that generate income through freight rates correlated with global trade volumes.

The economic characteristics of maritime asset investment include:

Income generation: Vessels on time charter generate daily hire income. Vessels on voyage charters generate freight income per voyage. The income profile resembles infrastructure in that it is contractually defined for the charter period.

Asset appreciation/depreciation: Vessel values fluctuate with newbuilding prices, scrap steel prices, and fleet supply/demand dynamics. Older vessels depreciate; vessels in periods of high demand may appreciate relative to their historical cost.

Low correlation with equities: Maritime freight rates are driven by global trade volumes, fleet supply, and port congestion. These drivers are distinct from the earnings cycles of listed companies. Shipping assets have historically shown low correlation with equity indices.

Market access: Until recently, maritime asset investment was accessible primarily to shipowners, shipping companies, and specialist maritime funds. Digital platforms using on-chain infrastructure to represent economic exposure to commercial vessels are expanding access to this asset class for a broader range of participants.

Shipfinex's Maritime Asset Tokens (MATs) represent economic exposure to commercial vessel Special Purpose Vehicles (SPVs), enabling platform participants to access maritime asset economics in a regulated structure without requiring direct vessel ownership.

FAQ On Alternative Investments

What are alternative investments?

Alternative investments are asset classes outside publicly traded stocks, bonds, and cash. They include private equity, hedge funds, real estate, infrastructure, private credit, commodities, and real assets. They are characterised by lower liquidity, limited public market correlation, and typically higher minimum investment requirements.

What are the main types of alternative investments?

Private equity (buyout, venture capital, growth equity), hedge funds, real estate (direct property, private funds, REITs), infrastructure, private credit, commodities, and real assets including maritime assets, timber, farmland, art, and precious metals.

What are the advantages of alternative investments?

Portfolio diversification through low equity correlation, return enhancement from illiquidity premiums, inflation hedging through real assets, access to private market returns, and stable income from infrastructure and real assets.

What are the disadvantages of alternative investments?

Illiquidity (capital locked for years), high minimum investment requirements, complexity and due diligence burden, high fee structures, limited transparency, regulatory complexity, and valuation uncertainty.

Who can invest in alternative investments?

In most jurisdictions, alternatives are restricted to accredited or sophisticated investors. In the US, the accredited investor standard requires net worth above $1 million or annual income above $200,000. Institutional investors (pension funds, sovereign wealth funds, endowments) are the primary allocators. Some tokenised or listed alternative structures lower the access threshold.

Are alternative investments high risk?

Risk varies enormously by asset class. Venture capital has very high loss rates with occasional exceptional returns. Infrastructure assets in regulated sectors have low fundamental risk. The common thread is that alternatives require specialist knowledge to evaluate, and the illiquidity means errors of judgement cannot be quickly corrected.

What is an illiquidity premium?

The additional return earned by investors in exchange for committing capital to illiquid assets. Because investors cannot access their capital on demand, they require higher expected returns than liquid equivalents. Private equity returns have historically included an illiquidity premium over public equity.

How are alternatives different from traditional investments?

Traditional investments (public stocks and bonds) trade on exchanges with continuous pricing, daily liquidity, and regulatory disclosure requirements. Alternatives are privately structured, infrequently priced, illiquid, and require active due diligence. They offer different return drivers and diversification benefits.

What is the "2 and 20" fee structure?

The standard alternative investment fund fee model: a 2% annual management fee on committed or invested capital, plus 20% carried interest (a share of profits above a specified hurdle rate). This model is used in PE and hedge funds; competitive pressure has reduced fees for some strategies.

What is private credit?

Private credit is lending to companies or projects outside the public bond market. It includes direct lending to mid-market companies, mezzanine debt, distressed debt, and trade finance. It emerged significantly after the 2008 financial crisis and offers floating-rate, higher-yield returns than equivalent public market fixed income.

How do maritime assets qualify as alternative investments?

Commercial vessels are physical, long-duration assets generating freight income driven by global trade dynamics rather than equity market sentiment. They have low correlation with public markets and require specialist knowledge to evaluate. They exhibit characteristics of both infrastructure (long-lived assets, contracted income) and commodities (exposure to freight market cycles).

How are alternative investments regulated?

Regulation varies by jurisdiction and asset class. In the US, the SEC regulates private funds under the Investment Advisers Act. In the UK, the FCA applies AIFMD (Alternative Investment Fund Managers Directive) rules. In the UAE, VARA and the FSRA regulate digital asset and some private fund structures. Investors must understand the regulatory framework of the specific jurisdiction and structure of each investment.

Glossary

Accredited investor: An individual or entity meeting regulatory net worth or income thresholds that permit participation in private investment offerings.

Buyout: A PE strategy involving acquisition of a controlling stake in a company, typically using debt, with the goal of improving and exiting the business.

Carried interest: The fund manager's share of profits above a hurdle rate, typically 20% in PE and hedge fund structures.

Closed-end fund: A fund with a fixed capital commitment period and a defined life, after which the fund distributes returns and terminates; standard structure for PE funds.

Commodities: Raw materials including agricultural products, energy resources, and metals; tradeable directly or through futures contracts.

Direct lending: Providing loans directly to companies, bypassing the bank lending market; the primary form of private credit.

Drawdown: The process by which PE funds call committed capital from investors as investment opportunities arise during the investment period.

Hedge fund: A pooled investment vehicle using a wide range of strategies (short selling, leverage, derivatives) to generate returns; typically requires significant minimum investment.

Hurdle rate: The minimum return that a PE or hedge fund must achieve before carrying interest becomes payable to the manager.

Infrastructure investment: Investment in physical assets providing essential services: transport, utilities, energy, digital infrastructure.

Illiquidity premium: The additional return earned by investors in exchange for committing capital to assets that cannot be quickly sold.

Limited partner (LP): The investor in a PE, infrastructure, or real estate fund; provides capital and has limited liability but no management role.

MAT (Maritime Asset Token): A digital token representing economic exposure to a commercial vessel SPV on the Shipfinex platform.

Mezzanine debt: Subordinated debt ranking below senior secured debt but above equity in the capital structure; commands higher interest rates to reflect higher risk.

Private equity (PE): Investment in non-publicly traded companies through buyout, growth equity, or venture capital strategies.

Real assets: Physical, tangible assets including real estate, infrastructure, maritime assets, timber, farmland, art, and precious metals.

REIT (Real Estate Investment Trust): A pooled vehicle holding real estate assets; listed REITs trade on stock exchanges; non-listed REITs are private.

SPV (Special Purpose Vehicle): A legal entity created for a specific purpose (such as owning a single vessel or a specific property); isolates the asset and its liabilities from the parent entity.

Venture capital: Early-stage investment in startups; high risk, potential for exceptional returns from successful companies.

References

Preqin: Global Alternatives Report 2024

CFA Institute: Alternative Investments: A Primer for Investment Professionals

Yale Investments Office: Endowment Reports (Yale Model / David Swensen)

Investopedia: Alternative Investments Overview

CFA Institute: Real Assets, Hedge Funds, and Alternatives

ILPA (Institutional Limited Partners Association): PE Fee and Expense Reporting Standards

Preqin: Private Debt and Infrastructure Market Data 2024

ARQ Wealth: 7 Alternative Investment Strategies for 2025

SoFi: What Are Alternative Investments? Definition and Examples

Manhattan West: A Guide to Alternative Investments 2025

Chambers and Partners: Alternative Funds Global Practice Guide 2025

World Bank: Infrastructure Finance and Private Investment

Disclaimer: Shipfinex FZCO operates under VARA In-Principle Approval (IPA/26/01/002). The final Virtual Asset Service Provider (VASP) license is pending. Maritime Asset Tokens (MATs) available on the Shipfinex platform represent economic exposure to commercial vessel Special Purpose Vehicles (SPVs) and are subject to regulatory review. This article is for informational purposes only and does not constitute financial or investment advice. Platform participants should consult qualified financial advisers and review all relevant offer documents and risk disclosures before making any financial decision.

Ravi Shanker

Co-Founder & CCO, Shipfinex

Ravi Shankar FICS is Co-Founder and Chief Commercial Officer of Shipfinex, and General Secretary of the ICS Middle East Branch. A Fellow of the Institute of Chartered Shipbrokers with extensive experience in ship sale and purchase, chartering, and maritime consultancy, he has previously held senior roles at Maersk Broker and Eastgate Shipping DMCC. His day-to-day commercial work spans dry bulk and tanker market analysis, SnP transactions, and shipbroking advisory.