P&I Insurance Explained: What It Covers, What It Doesn’t

- Capt. Anuj Chopra

- Jun 15

- 21 min read

Updated: Jun 19

Most articles on P&I insurance tell you what it covers. None of them tell you what it does not cover, why some vessels operating right now have no usable cover at all, or what happens when an insurer withdraws cover from an entire trade.

I spent nearly a decade at RightShip evaluating exactly these type of questions on behalf of cargo owners, charterers, and ports. P&I quality, certificate validity, and club recognition were professional inputs I used daily to assess vessel risk. This is the version written from that desk.

Who this guide is for: Shipowners, operators, senior officers, maritime finance professionals, charterers, and anyone who needs to understand P&I beyond a definition, including what it excludes, how pooling works, and what the withdrawal of Western club cover from the sanctioned trade means for vessels operating today.

Quick Answer: P&I (Protection and Indemnity) insurance is a mutual marine liability policy covering a shipowner’s third-party liabilities: crew injury and death, cargo loss, pollution, collision damage to third-party property, wreck removal, and port entry compliance certificates. It is provided primarily by the 12 clubs of the International Group of P&I Clubs, which together cover approximately 90% of the world’s ocean-going tonnage.

What Is P&I Insurance and Why Does It Exist

Think of a shipowner like a truck driver. The truck policy covers damage to the truck itself. It does not cover the damage the truck causes to a pedestrian, another vehicle, or a building it hits. For that, the driver needs a separate liability policy.

Hull and Machinery (H&M) insurance covers the vessel. Protection and Indemnity (P&I) insurance covers the owner’s liability to everyone else: crew members who are injured, cargo owners whose goods are damaged, coastal communities affected by a pollution spill, and port authorities who must remove a sunken wreck.

The reason P&I exists as a separate category traces back to 1854. The British Merchant Shipping Act imposed new third-party liabilities on shipowners that went well beyond what commercial marine insurers were willing to write at the time. Shipowners formed mutual Protection Clubs to fund these liabilities collectively. Twenty years later, separate Indemnity Clubs formed to cover contractual cargo liabilities under bills of lading.

In 1874 the two merged. By 1884, five original clubs had entered into the first pooling agreement, sharing large claims among themselves. The Shipowners’ Club is one of those five original clubs, making it one of the oldest continuously operating P&I organizations in the world.

The Origin of the “Protection” and “Indemnity” Names

“Protection” originally referred to statutory liabilities: the obligations imposed on shipowners by law for personal injury, loss of life, and collision damage. “Indemnity” referred to contractual liabilities: the obligations shipowners undertook under bills of lading and charterparties for cargo. Today the distinction is largely historical. Modern P&I clubs cover both statutory and contractual liabilities under a single club entry. But understanding the origin explains why P&I covers such a broad range: it was always designed to be the liability policy of last resort for everything the H&M policy did not cover.

Why Commercial Insurers Could Not Fill This Role

P&I liabilities are open-ended and potentially catastrophic. A major pollution event costs hundreds of millions to a billion or more to clean up and compensate. The Prestige tanker off Spain in 2002 and the Erika off France in 1999 each sat in this range. A casualty involving multiple fatalities, total cargo loss, and wreck removal in a major shipping lane can run to comparable sums.

No commercial insurer is willing to write unlimited liability cover at a fixed premium for risks of this scale. The mutual model, where member shipowners collectively fund claims through calls adjusted each policy year, is the only sustainable structure. This is why approximately 90% of the world’s ocean-going tonnage remains with the 12 mutual clubs of the International Group rather than with commercial fixed-premium alternatives.

How P&I Clubs Work: The Mutual Model Explained

A P&I club is owned by its members, not by shareholders. Every shipowner or charterer who enters a vessel with a club becomes a member of that club. They elect a board of directors from among themselves. The club has no external investors, pays no dividends, and takes no commercial profit. Surplus from a good claims year goes into free reserves or is applied to reduce future calls. The aggregate free reserves held across the 12 IG clubs currently exceed $4 billion.

How Calls Are Calculated

Premiums in a P&I club are called “calls,” not premiums. The distinction matters. At the start of each policy year (which runs from 20 February), the club estimates what the year’s total claims will cost across the membership. It sets an advance call for each member based on the gross tonnage of vessels entered, the risk profile of those vessels (type, age, trade, flag), the member’s individual claims history, and the cargo types and trade routes covered.

A tanker owner with a history of pollution incidents pays a different rate than a bulk carrier owner on clean trades. A vessel operating in sanctions-risk regions carries a higher risk profile than one on established trade routes.

The Policy Year and the 20-Year Tail

P&I policies run on a policy year basis. The policy year closes on 20 February each subsequent year. But claims from a closed policy year can still be reported and resolved years or decades later. A crew member who suffered a serious injury on a 2019 voyage may pursue a compensation claim into 2026 or beyond. A cargo contamination claim may take five years to work through the courts.

This long tail explains why P&I clubs maintain free reserves far in excess of their annual advance calls. They are always holding funds against claims from policy years that technically closed years ago.

How a P&I call works, step by step:

1. Club estimates total claims for the policy year

2. Advance calls are set per member based on tonnage and risk profile

3. Members pay advance calls, typically in quarterly installments

4. Claims are paid throughout the year from the pooled fund

5. At year end, actual claims are compared against estimates

6. If claims exceed estimates, a supplementary call is issued

7. Surplus years contribute to free reserves held for future years

The supplementary call is the feature that distinguishes mutual P&I from commercial insurance most sharply. Members cannot budget for a completely fixed annual P&I cost. In a bad claims year, a major casualty or a catastrophic pollution event, every member of the club shares the additional cost through a supplementary call.

What P&I Insurance Covers: The Full Liability Spectrum

Every competitor article lists P&I coverage. What most miss is why each category exists and how large the claims can run.

Crew Liabilities

Personal injury, illness, and death of crew members, including medical treatment, repatriation, and compensation under employment contracts. The Maritime Labour Convention 2006 (MLC) has standardized minimum compensation across most flag states. For a vessel with a mixed Asian and Eastern European crew of 25, a serious casualty involving multiple fatalities can generate $5 million or more in P&I crew liability claims alone, before legal costs.

Cargo Liabilities

Damage to or loss of cargo while in the shipowner’s custody under a bill of lading. The cargo’s own insurer pays the cargo owner, then pursues a subrogated recovery claim against the shipowner. P&I covers that subrogated claim. A container ship losing a deck stack in heavy weather may face cargo claims from dozens of individual cargo interests. A bulk carrier contaminating a grain cargo through water ingress may face a single large claim from a grain trading house.

Collision and Property Damage

Damage caused by the vessel to third-party property: other vessels, jetties, navigational buoys, port infrastructure, and offshore structures. A Capesize vessel alliding with a jetty in a major Australian port can generate tens of millions in jetty damage costs, including the consequential economic loss to the port from the closure and repair period.

Pollution

Oil spills, chemical releases, and other hazardous substance discharges. P&I covers cleanup costs, fines and penalties from regulatory authorities, and compensation claims from affected communities and businesses. The Civil Liability Convention (CLC) imposes strict liability on tanker owners for oil pollution. The Bunker Convention imposes strict liability on all vessel types for bunker fuel spills.

Wreck Removal

If a vessel sinks and constitutes a navigation hazard, port authorities can issue a compulsory removal order under the Nairobi International Convention on Wreck Removal (in force 2015). The cost of removing a large vessel from a busy shipping channel can run to $50 million or more. P&I covers this liability once H&M insurers have agreed to pay a Constructive Total Loss on the hull.

Fines and Legal Costs

Fines imposed by port authorities, coast guards, or customs officials for breach of regulations including accidental MARPOL violations, load line infringements, and document irregularities. P&I also covers the cost of mounting a legal defence, engaging surveyors, and pursuing recovery against third parties.

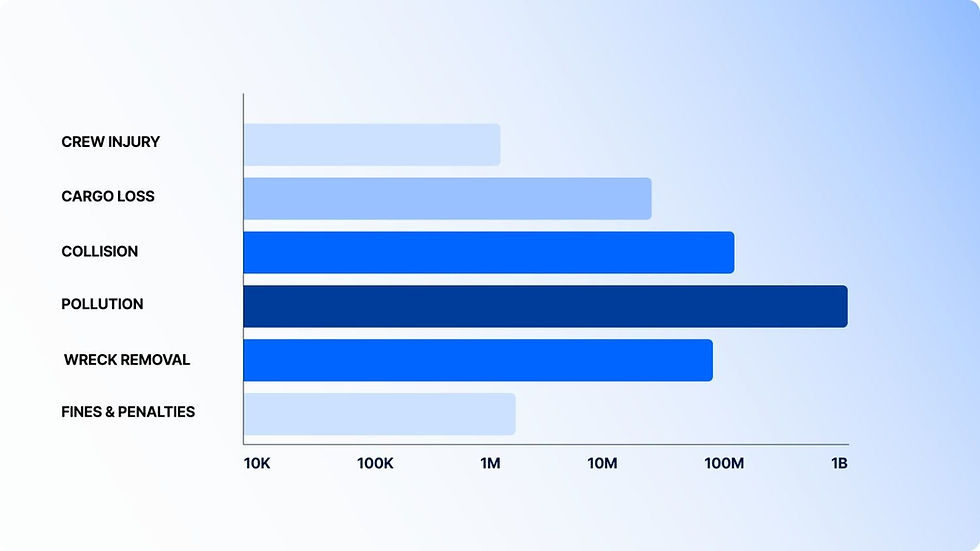

Coverage Category | Legal Basis | Typical Claim Scale |

Crew injury, illness, death | Employment contract, MLC 2006 | $50K to $2M+ per crew member |

Cargo loss or damage | Bill of lading, Hague-Visby Rules | $100K to $50M+ |

Collision (1/4 + excess above H&M) | Maritime law | $1M to $500M+ |

Pollution (oil, chemical) | CLC, Bunker Convention, MARPOL | $1M to $1B+ |

Wreck removal | Nairobi Convention | $5M to $200M+ |

Fines and penalties | Port state and flag state regulations | $10K to $5M+ |

Legal costs and defence | Club rules | Variable |

What P&I Insurance Does Not Cover: The Exclusions Every Owner Must Know

No competitor article covers this. It is the most commercially useful thing I can add to this topic.

P&I is not all-encompassing maritime liability cover. Every club’s rules contain defined exclusions. An owner who does not know these exclusions has an uninsured exposure they may not discover until they need to make a claim.

War Risk and Named Perils

P&I does not cover war risk, acts of war, piracy in some circumstances, or political violence. A vessel caught in a military conflict, detained by a state actor, or attacked by armed groups needs separate war risk cover from the commercial marine war market. This distinction became operationally significant for vessels operating in the Red Sea after the Houthi attacks began in late 2023, and for vessels in the Black Sea during the Ukraine conflict. An owner who lets war risk cover lapse while operating in a high-risk region has no P&I club standing behind them for war-related casualties.

Wilful Misconduct and Sanctions Violations

No P&I club will pay a claim arising from the owner’s deliberate wilful misconduct. Knowingly loading sanctioned cargo, calling at sanctioned ports in breach of applicable law, or transporting goods in violation of OFAC, EU, or UK sanctions falls into this category. The club’s rules exclude it, and the club’s reinsurers exclude it. An owner who deliberately breaches sanctions and then suffers a casualty will find their P&I claim denied.

Hull Damage to Own Vessel

P&I covers nothing for damage to the insured vessel itself. A vessel that collides with another and suffers $10 million in hull damage has a claim on its H&M policy for that damage, not its P&I club.

Nuclear, Chemical, Biological, and Radiological Incidents

All IG club rules exclude nuclear incidents, radioactive contamination, and CBRN events. These risks are uninsurable in the mutual insurance market.

Cargo Owned by the Shipowner

If an owner is also carrying their own cargo (integrated operator), P&I does not cover damage to that cargo. Separate cargo insurance is required for the owner’s own goods.

P&I and Hull and Machinery Insurance: How the Two Policies Fit Together

These two policies are not alternatives. They are complementary layers that a shipowner must hold simultaneously to be fully covered and compliant.

What H&M Covers

Hull and Machinery (H&M) insurance covers physical damage to the vessel itself: collision damage to own ship, machinery breakdown, fire, grounding, explosion, and other named perils. H&M is a commercial insurance policy placed through Lloyd’s of London or other commercial marine insurers at a fixed premium.

The 3/4 Collision Liability Split

Under standard H&M policies using the Institute Time Clauses - Hulls (ITC-H), the H&M policy covers 3/4 of the shipowner’s liability for damage caused to another vessel in a collision. The P&I club covers the remaining 1/4, plus any collision liability that exceeds the insured value of the H&M policy.

This split exists because it was the established commercial practice when the ITC-H form was drafted. Some P&I clubs, including Maritime Mutual, now offer “4/4 collision” cover entirely under P&I, eliminating the split and simplifying claim adjustment.

Why does the split matter? If a vessel worth $20 million on its H&M policy collides with and totally destroys a vessel worth $80 million, the H&M policy covers $15 million (3/4 of $20M cap). The P&I club covers the remaining $65 million. Without adequate P&I capacity, the owner has an uncovered gap of tens of millions.

Coverage Layer | H&M (Hull and Machinery) | P&I (Protection and Indemnity) |

Own vessel physical damage | YES | NO |

Third-party vessel collision damage | 3/4 (standard) | 1/4 + excess |

Crew personal injury | NO | YES |

Third-party cargo liability | NO | YES |

Pollution liability | Limited | YES |

Wreck removal | NO (post-CTL) | YES |

Port entry compliance certificates | NO | YES |

MLC Certificates and Blue Cards: The Port Entry Compliance Layer

This is the P&I layer most shipowners understand least and discover most expensively when it fails.

MLC Certificates of Financial Security

The Maritime Labour Convention 2006 requires every ship over 500 gross tonnes engaged in international trade to carry two separate MLC Certificates of Financial Security. These are not optional documents; they are port entry requirements.

Certificate 1 covers repatriation and unpaid wages under MLC Regulation 2.5. If a shipowner becomes insolvent and abandons crew, this certificate guarantees that a recognized financial security provider (the P&I club) will pay for crew repatriation and outstanding wages.

Certificate 2 covers compensation for death and long-term disability under MLC Regulation 4.2. This certificate confirms that in the event of a serious injury or fatality, the owner’s financial security provider will pay the statutory compensation.

Both certificates must be issued by an approved insurer, displayed on board, and available for Port State Control inspection. A vessel without valid MLC Certificates can be detained. PSC inspectors in Paris MoU, Tokyo MoU, and USCG regimes check for these as standard inspection items.

CLC and Bunker Convention Blue Cards

The Civil Liability Convention (CLC) applies to tankers carrying oil in bulk. The Bunker Convention applies to all vessels over 1,000 gross tonnes. Both require the vessel’s flag state to issue a trading certificate confirming that liability insurance meeting convention standards is in place. The flag state issues that certificate only when the owner presents a “Blue Card” from an approved insurer confirming coverage.

Without a valid Blue Card, no flag state certificate. Without a flag state certificate, no legal entry into convention state ports. For a commercial vessel, this means no trade.

Convention | Certificate Required | Consequence Without Valid Cover |

MLC 2006 (Reg. 2.5) | Certificate of Financial Security (repatriation) | PSC detention |

MLC 2006 (Reg. 4.2) | Certificate of Financial Security (death/disability) | PSC detention |

CLC (oil tankers) | Flag State CLC Certificate (from Blue Card) | Port entry refused |

Bunker Convention (all vessels 1,000+ GT) | Flag State Bunker Certificate (from Blue Card) | Port entry refused |

Nairobi Wreck Removal Convention | Wreck removal insurance certificate | Port entry refused |

The practical message for a shipowner: the moment your P&I cover is cancelled, suspended, or held by an insurer not recognized by convention states, you may lose port access before you lose anything else.

The International Group: Pooling, Reinsurance, and the $10 Million Threshold

The IG structure is the mechanism that makes billion-dollar P&I claims coverage possible.

Individual Club Retention and the Pool

Each of the 12 IG member clubs covers claims from its own reserves up to its individual retention limit, currently set at $10 million per claim. Claims above $10 million enter the pooling arrangement, where they are shared among all 12 clubs in proportion to their entered tonnage.

Above approximately $100 million, the IG’s Group Excess of Loss reinsurance contract (GXL) takes over. The GXL is placed annually in the commercial reinsurance market, with Lloyd’s syndicates and international reinsurers as the counterparties. The total coverage capacity available through the IG system runs to approximately $3 billion per claim.

Why Pooling Enables Catastrophic Coverage

No single mutual club could absorb a $1 billion pollution claim from its own reserves. Gard has approximately $500 million in free reserves. UK P&I Club, West of England, and Britannia are in similar ranges. A catastrophic claim at the top of the scale would threaten any individual club’s solvency if it had to bear it alone.

By pooling claims above the individual retention, the 12 clubs collectively back each other’s catastrophic losses. Port states and convention signatories accept IG club Blue Cards precisely because they know that behind every IG club stands the collective capacity of the entire Group.

The Annual GXL Reinsurance Renewal and Its Sanctions Implication

The GXL is renewed every year. In 2022, commercial reinsurers introduced broad sanctions exclusions into their GXL offerings. Russian-related risks, sanctioned entities, and vessels above the G7 oil price cap were excluded from the reinsurance contract. The consequence for IG clubs was direct: they could not maintain cover for trades that their own reinsurance excluded. The clubs did not choose to withdraw for political reasons. Their reinsurance contract left them no alternative.

Fixed Premium vs Mutual P&I: What the Difference Means in Practice

Dimension | IG Mutual Club | Fixed Premium Insurer |

Premium structure | Estimated calls + potential supplementary | Fixed premium, no supplementary call |

Coverage capacity | Up to ~$3B via pool and GXL | Limited by insurer’s own capital |

Convention certificate recognition | Accepted globally | Varies by insurer and convention |

Claims expertise | Deep maritime specialization | Variable |

Supplementary call risk | Yes, in a heavy loss year | No |

Loss prevention services | Included | Rarely included |

Who uses it | ~90% of ocean-going tonnage | Smaller vessels, specific trades |

Fixed premium P&I suits owners of smaller vessels, those on well-defined low-risk trades, and operators who cannot absorb supplementary call uncertainty in their cash flow. The tradeoff is coverage capacity and certificate recognition. Not all fixed premium insurers are recognized by convention states as approved issuers of MLC Certificates or Blue Cards. An owner who selects a fixed premium provider without checking convention recognition may find their vessel unable to enter certain ports.

When Western P&I Clubs Withdrew: Sanctions, the Shadow Fleet, and the Cover Gap

Nothing in this section exists in the current SERP. It is the section that makes this article genuinely useful to anyone operating in or evaluating vessels active in current global trade.

What Actually Happened in 2022

Following Russia’s invasion of Ukraine and the imposition of comprehensive EU, UK, and US sanctions in February and March 2022, the IG clubs began a structured withdrawal from cover for vessels and cargo falling within the sanctions perimeter. The withdrawal was not spontaneous. Each club issued notice under their rules (typically 30 days) and worked with members to clarify which vessels, cargoes, and routes remained outside the sanctions scope.

The underlying mechanism was the GXL reinsurance contract. When Lloyd’s and international reinsurers introduced sanctions exclusions into their annual renewals, the IG clubs’ own reinsurance no longer covered sanctioned trades. A club continuing to provide cover for a sanctioned trade was doing so without the backing of its reinsurance programme. No club board was willing to take on that unprotected exposure for its membership.

By mid-2022, IG clubs had largely withdrawn from: cover for vessels owned by sanctioned Russian entities, cover for cargoes that violated the G7 oil price cap, and cover for voyages to and from certain sanctioned Russian ports.

What the Shadow Fleet Actually Carries

The shadow fleet (estimated at 600 or more vessels as of 2026) operates with one of three insurance arrangements. The Russian National Reinsurance Corporation (NSR) was established by the Russian government specifically to backstop maritime insurance following Western withdrawal. NSR provides reinsurance to Russian insurers, primarily Ingosstrakh. Ingosstrakh issues P&I-equivalent policies to shadow fleet vessel operators. Some vessels carry coverage from obscure insurers registered in Gabon, Cameroon, or other jurisdictions.

The fundamental problem is not whether these insurers pay claims. It is whether their coverage satisfies convention requirements. NSR and Ingosstrakh are not recognized by the majority of convention state authorities as approved issuers for CLC Blue Cards, Bunker Convention certificates, or MLC Certificates of Financial Security. A vessel holding only Russian-sourced insurance documentation cannot legally enter most EU, UK, US, or major Asian ports.

The Port Entry Consequences

A shadow fleet vessel attempting to call at an EU port faces this sequence: the flag state (often Panama, Palau, Cook Islands, or Gabon) may or may not have issued a CLC certificate backed by NSR. If the flag state did issue one, the convention state port authority may challenge its validity. PSC inspectors check for valid flag state certificates. If the certificate references an approved insurer who has since been sanctioned or whose recognition has been withdrawn, the certificate is effectively invalid.

The vessel is either refused entry or detained. The owner has to arrange replacement documentation from a recognized insurer before the vessel can sail. For a vessel deeply embedded in the shadow fleet, that replacement cover is unavailable from any IG club.

The Third-Party Risk: Who Pays When Things Go Wrong

The conventions exist to protect coastal communities and governments from the cost of uninsured maritime casualties. The Prestige spill off Spain in 2002 cost over $1 billion in cleanup and compensation. Spain was able to recover much of this through the IOPC Fund, which is backed by cargo interests and operates alongside CLC. That recovery mechanism requires valid CLC cover in the first place.

A shadow fleet tanker carrying Russian crude that suffers a major blowout off a European coastline with only NSR cover presents a different recovery picture. The coastal state faces a much harder path to compensation. The IOPC Fund contribution from sanctioned cargo interests may be contested. NSR’s actual payment capacity and willingness in a cross-border claim involving a Western state is an open question.

This is not theoretical. Collisions involving shadow fleet vessels have already occurred in the Baltic, Black Sea, and North Sea. Each one is a test case for what the insurance gap means when something actually goes wrong.

P&I, Vetting, and Port State Control: The Compliance Chain

What Vetting Organizations Look for in P&I

When RightShip assigns a vessel a GHG rating or a safety score, P&I club membership is a positive signal in the overall assessment. IG club membership tells a vetting professional three things.

First, the vessel has been accepted on cover by a technical organization that reviews vessel condition and claims history before granting entry. Clubs can and do decline to enter vessels they consider too high-risk. IG membership is a basic quality filter.

Second, the owner has access to loss prevention expertise from a team of maritime lawyers, surveyors, and technical specialists whose full-time job is to help members avoid incidents.

Third, the vessel’s third-party liability is backed by the full IG pool capacity, meaning that if this vessel causes a major incident, the affected parties can recover.

Oil majors and major commodity trading houses routinely require IG club membership as a condition of chartering a vessel. A vessel without IG cover, or with cover from a non-recognized insurer, is effectively shut out of the better-quality charter markets.

PSC Detention for Insurance Non-Compliance

Paris MoU, Tokyo MoU, and USCG inspectors check for MLC Certificates and flag state CLC/Bunker certificates as standard inspection items. If a vessel arrives with expired certificates, certificates from a non-recognized insurer, or missing documentation entirely, the inspector issues a deficiency and the vessel cannot sail until the deficiency is rectified.

For a vessel under a time charter, every day of PSC detention for insurance non-compliance is a day of off-hire. The owner bears the cost. The charterer may have grounds to terminate the charterparty if the detention is prolonged. Beyond the commercial cost, repeated insurance-related PSC deficiencies will damage the vessel’s PSC inspection history, pushing it further down the quality rankings that RightShip and similar organizations maintain.

The compliance chain is: adequate P&I cover from a recognized insurer issues correct documentation, the flag state issues the required certificates, PSC inspectors find the certificates valid, the vessel trades without interruption. Every link in that chain must hold.

Frequently Asked Questions

What is P&I insurance in shipping?

P&I insurance, short for Protection and Indemnity insurance, is a mutual marine liability policy that covers shipowners and operators against third-party legal liabilities arising from the operation of their vessels. It covers crew injury and death, cargo damage and loss, collision damage to other vessels and property, pollution, wreck removal, and fines and legal costs. It is provided primarily by the 12 mutual clubs of the International Group of P&I Clubs, which together cover approximately 90% of the world’s ocean-going tonnage.

What does P&I insurance cover?

P&I covers crew liabilities including personal injury, illness, and death; cargo liabilities including damage to and loss of third-party cargo under bills of lading; collision damage to other vessels and third-party property; pollution cleanup costs and fines; wreck removal under compulsory port authority orders; and legal costs of defending or pursuing maritime claims. It also issues the compliance documentation (MLC Certificates and Blue Cards) required for port entry under international conventions.

What does P&I insurance not cover?

P&I does not cover war risk (requiring a separate policy), hull damage to the insured vessel (covered by H&M), the owner’s own cargo, nuclear or CBRN incidents, or claims arising from wilful misconduct or deliberate sanctions violations. The exclusions in each club’s rules define the limits of coverage and differ slightly by club.

What is the International Group of P&I Clubs?

The International Group (IG) is an unincorporated association of 12 independent, not-for-profit mutual P&I clubs that collectively cover approximately 90% of the world’s ocean-going tonnage. The IG’s primary function is operating the claims pooling agreement (which shares large claims above each club’s individual $10 million retention across all 12 clubs) and placing the annual Group Excess of Loss reinsurance contract that covers pool claims above approximately $100 million.

How is a P&I call different from a premium?

A commercial insurance premium is fixed in advance and does not change regardless of how many claims occur during the year. A P&I call is an estimate at the start of the policy year of the member’s share of the club’s anticipated total claims cost. If claims in the year exceed estimates, the club can issue a supplementary call to all members. In a good year, surplus funds go to free reserves. The supplementary call risk is the main practical difference between mutual P&I and fixed premium commercial insurance.

What is the difference between P&I and Hull and Machinery insurance?

H&M insurance covers physical damage to the vessel itself: collision damage to own ship, grounding, fire, machinery breakdown. P&I covers the owner’s liabilities to third parties: cargo owners, crew members, other vessels, coastal communities. The two policies are complementary, not alternatives. A vessel without both has uncovered exposures. Under standard H&M policy terms, H&M covers 3/4 of the owner’s collision liability to third-party vessels; P&I covers the remaining 1/4 plus any excess above the H&M insured value.

What is an MLC Certificate of Financial Security?

The Maritime Labour Convention 2006 requires every vessel over 500 gross tonnes in international trade to carry two MLC Certificates of Financial Security: one covering repatriation and unpaid wages (Regulation 2.5), and one covering compensation for death and long-term disability (Regulation 4.2). These certificates are issued by the vessel’s P&I club or an approved alternative insurer. PSC inspectors check for them as standard items. A vessel without valid MLC Certificates can be detained in port.

What is a Blue Card in P&I insurance?

A Blue Card is a document issued by a P&I club confirming that a vessel has liability insurance meeting the requirements of a specific maritime convention (typically the CLC for oil tankers, the Bunker Convention for all vessels over 1,000 GT, or the Nairobi Wreck Removal Convention). The flag state requires the Blue Card to issue the vessel’s trading certificate under each convention. Without a Blue Card from a recognized insurer, there is no flag state certificate, and the vessel cannot legally enter ports in convention states.

Why did Western P&I clubs stop covering Russian vessels?

Western P&I clubs withdrew from the Russian sanctioned trade because their commercial reinsurance contracts excluded it. When Lloyd’s syndicates and international reinsurers introduced sanctions exclusions into the Group Excess of Loss reinsurance contract in 2022, IG clubs could no longer provide reinsured coverage for vessels and cargoes falling within the sanctions perimeter. Continuing to cover sanctioned trades would have meant the clubs bearing catastrophic loss exposure without reinsurance backing, which no club board was willing to accept on behalf of its membership.

What insurance do shadow fleet vessels carry?

Shadow fleet vessels typically carry insurance from the Russian National Reinsurance Corporation (NSR), from Ingosstrakh (the primary Russian marine insurer), or from obscure insurers in non-Western jurisdictions. The fundamental problem is that these insurers are not recognized by most convention states as approved issuers of CLC Blue Cards, Bunker Convention certificates, or MLC Certificates of Financial Security. A vessel holding only Russian-sourced insurance cannot legally enter most EU, UK, US, or major Asian ports, and the third-party recovery mechanism breaks down in the event of a major incident.

What happens if a vessel has no valid P&I cover?

A vessel without valid P&I cover from a recognized insurer loses access to the Blue Cards and MLC Certificates required for port entry under international conventions. It cannot legally enter most significant commercial ports. If the vessel is under a time charter, PSC detention for insurance non-compliance puts it off-hire at the owner’s expense. Oil majors and major charterers will not fix it. In the event of a casualty, the owner has no third-party liability cover for crew claims, cargo claims, or pollution cleanup costs.

Glossary of P&I and Marine Insurance Terms

Protection and Indemnity (P&I) insurance: Mutual marine liability insurance covering a shipowner’s third-party liabilities arising from vessel operation.

P&I Club: A mutual, not-for-profit insurance association owned and governed by its shipowner and charterer members.

International Group of P&I Clubs (IG): An unincorporated association of 12 independent P&I clubs that collectively cover approximately 90% of the world’s ocean-going tonnage.

Mutual insurance: An insurance model in which the policyholders (members) are also the owners of the insurer. No external shareholders. Surplus funds are returned to members or held as free reserves.

Call: The P&I equivalent of a premium. An estimated contribution by each member to the club’s anticipated annual claims cost.

Supplementary call: An additional call issued to members when a policy year’s claims exceed the advance call estimates.

Free reserves: Funds held by a P&I club beyond what is needed to pay anticipated claims from open policy years. IG club aggregate free reserves exceed $4 billion.

Pooling agreement: The agreement among the 12 IG clubs to share claims above each club’s individual retention threshold ($10 million per claim).

Group Excess of Loss (GXL) reinsurance: The annual reinsurance contract placed collectively by the IG clubs to cover pool claims above approximately $100 million. Total IG coverage capacity is approximately $3 billion per claim.

Hull and Machinery (H&M) insurance: Commercial insurance covering physical damage to the vessel itself. Does not cover third-party liabilities.

3/4 collision liability: The standard H&M policy term covering 3/4 of the owner’s liability for damage caused to another vessel in a collision.

Fixed premium P&I: P&I insurance placed with a commercial insurer at a fixed annual premium, with no supplementary call risk.

MLC Certificate of Financial Security: One of two certificates required under the Maritime Labour Convention 2006 for vessels over 500 GT in international trade.

Blue Card: A document issued by a P&I club confirming that liability insurance meeting a specific convention’s requirements is in place.

Civil Liability Convention (CLC): IMO convention imposing strict liability on tanker owners for oil pollution damage.

Bunker Convention: IMO convention imposing strict liability on all vessels over 1,000 GT for bunker fuel spill damage.

Nairobi Convention: The Nairobi International Convention on Wreck Removal (2007, in force 2015).

Port State Control (PSC): Inspection regime under which coastal states inspect foreign-flagged vessels in their ports to verify compliance with international conventions.

Correspondent: A P&I club’s local representative in a port or region, providing immediate on-the-ground assistance with surveying, claims, and regulatory response.

War risk insurance: Separate marine insurance covering damage or loss from war, acts of war, piracy, and political violence.

Russian National Reinsurance Corporation (NSR): A reinsurance entity established by the Russian government to backstop Russian maritime insurance. Not recognized by most convention states as an approved insurer for CLC or MLC certificates.

Shadow fleet: Vessels operating outside the Western insurance and vetting framework. Estimated at 600 or more vessels in 2026.

Constructive Total Loss (CTL): An H&M insurance determination that the cost of repairing a vessel exceeds its insured value.

Policy year: The 12-month period from 20 February during which a P&I policy is in force.

References

Disclaimer:This communication is issued by Shipfinex FZCO, operating under VARA In-Principle Approval (IPA/26/01/002). An IPA is not a full operational licence and is subject to completion of final regulatory requirements. Maritime Asset Tokens (MATs) are VARA-regulated virtual assets representing economic exposure to vessel-owning Special Purpose Vehicles. MATs are backed by real-world maritime assets (vessels) with intrinsic underlying value, including residual scrap and salvage value; however, MAT values may decline materially below the price at which they were purchased, and you may receive less than your invested amount including after accounting for income received. Distributions depend on vessel performance, charter status, operating costs, and SPV board declaration and are not guaranteed. Do not invest amounts you cannot afford to lose. This communication does not constitute financial, investment, or legal advice. Prospective MAT holders should review the full offering documentation and seek independent professional advice before making any purchase decision.

Capt. Anuj Chopra

Advisor / Contributing Author

Capt. Anuj Chopra ExC FNI FICS is a maritime industry executive with over 40 years of experience. As former VP Americas at RightShip and co-founder of ESGplus LLC, he specialises in maritime risk, ESG, and environmental compliance. He is an Adjunct Professor at the University of Houston and Fellow of both The Nautical Institute and the Institute of Chartered Shipbrokers.